LOOKING ON THE BRIGHT SIDE

Just as the City of Lake Geneva appeared to be blocked from spending any more Tax Increment District #4 (TID#4) money, an audit of TID#4 by Schenck Accounting Firm found $6 million and a legal opinion from the city’s attorney could possibly “OK” the city to spend it. Something doesn’t smell right, but how foul is it?

First:

Schenck points out that the management of Lake Geneva is responsible for the financial data presented (not Schenck). So how did the city manage to find $6 million dollars to spend? Answering this question involves comparing other city records with the Schenck Audit spreadsheet. Currently TID#4 operates under the 2010 amendment #3 which approved the city to expend a total project cost of $23,695,246. That figure is the combination of the TIF#4 costs thru April, 2009 of $7,566,046 plus an additional $16,451,200 in TIF#4 spending. With the city having spent $21,129,723 it can only spend $2.6 million more.

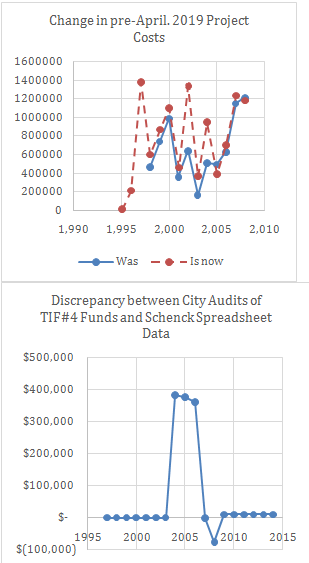

However, in the new spreadsheet in which the $6 million dollars is identified, the city changed the city’s “Reported Project Costs” of $7,566,046 thru April, 2009 to “Actual Project Cost” of $10,747,504. A $3.4 million increase. The new numbers include interest, debt and insurance costs which sounds legitimate; however, by doing this it also implied (which was then assumed) the maximum TIF#4 spending limit should also be increase by the same $3.4 million. That assumed increase in maximum spending, combined with the $2.6 million categorized unspent but authorized spending of TIF#4 money opened the possibility for the city to spend up to $6 million out of TIF#4 fund ($2.6 million + $3.4 million = the $6 million).Other changes/discrepancies were also found between previous city data and Schenck data. The money in the TIF#4 fund as recorded in the City Audits does not always agree with the data in the Schenck spreadsheet. In three years they varied by around $350,000 and 7 others years they varied from $10 thousand to $75 thousand as shown below.

Are these changes legitimate changes to correct previous error and are they within the intent of the approved TID#4 spending limit or is this just another clever manipulation of financial data to get more money for the city to spend? Your answer to that question may depend on your level of trust of the city’s management.

With the city’s history of co-mingling of accounts, putting accounts within accounts and keeping things fluid with money borrowed and owed between accounts, it makes it difficult to track city money or to trust city government’s handling of it. Even tracing the $600,000 gift from Ryan Corporation (Target) into the TIF#4 account was confusing. The city shows it as a lump sum being deposited in TIF #4, but in a last hour change to a city resolution, the city used the same $600,000 [although not listed as that gift] to pay selected assessments of several owners along the Edwards Blvd Extension on its way into the TID#4 fund (how cleaver).

Does the current audit include the still unpaid Edwards Blvd assessments that are interest free and not due until after TID #4 closes?

There are many unanswered questions about the $6,000,000

and the spending of TID#4 money.

More Bright Side

The guy with the thumb and significant tummy in red was tooling about in his SUV with his girlfriend. He spotted an open parking spot on the opposite side of Center Street across from Starbucks on Monday afternoon. He flipped the car around, crossing the double yellow line to pull a U-turn and knocked the old gentleman riding his scooter onto the pavement. Nobody was hurt although the police were called, likely because of the old gentleman’s age and the fact that he looked exactly like the spitting image of Wisconsin itself.

Your thoughts on Bookeeping Practices?